Lyle Solomon, Attorney*

Committing to a Chapter 13 repayment plan means agreeing to three to five years of structured monthly payments under court supervision. That is a long time. And life rarely cooperates with court schedules. A sudden job loss, a serious medical diagnosis, or an unexpected divorce can trigger a Chapter 13 income drop severe enough to make your court-approved payments completely unmanageable. The good news is that federal bankruptcy law anticipates exactly this scenario and provides several legal remedies before your case collapses entirely.

Before exploring those remedies, recognize the warning signs that demand immediate legal attention:

- Missing even a single scheduled trustee payment

- Receiving a motion to dismiss filed by the bankruptcy trustee

- Relying on credit cards to cover everyday living expenses like groceries or utilities

- Facing an imminent change in employment, such as a layoff notice or a long-term disability diagnosis

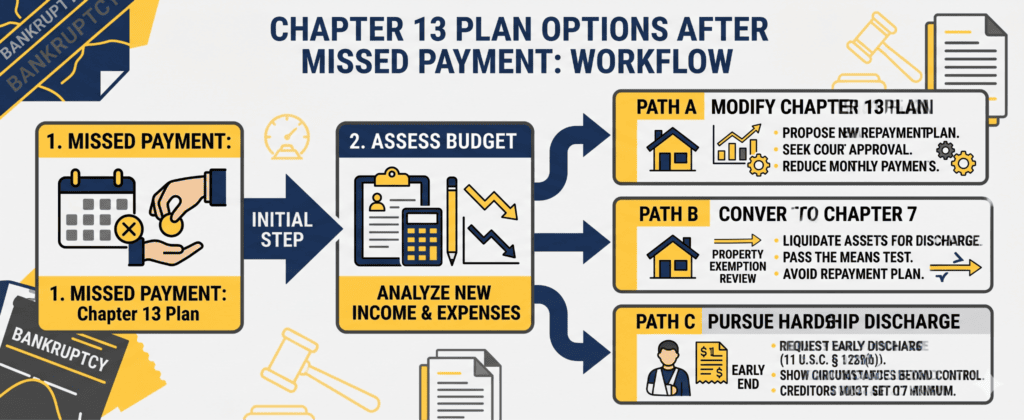

Option 1: How to Modify Your Chapter 13 Plan

Under 11 U.S.C. § 1329, federal bankruptcy law gives debtors the explicit right to formally request a plan modification when their financial circumstances change substantially. A successful modification can reduce your monthly plan payment to a level that reflects your new, lower income—without forcing you to abandon the bankruptcy relief options available to you under your existing case. According to the American Bankruptcy Institute, plan modifications are among the most commonly used tools by debtors experiencing mid-case financial disruption.

However, modification is not a blank check. The court imposes strict boundaries on what can and cannot be adjusted:

- Priority debts—including recent tax obligations and child support arrears—must still be paid in full, regardless of the modification

- Secured debt arrears, such as mortgage arrears, generally cannot be reduced if you intend to keep the property

- The modified plan must still be completed within the original 3-to-5-year term—the court will not extend the deadline indefinitely

- You must submit documented proof of the income drop, including termination letters, medical bills, disability determinations, or employer notices

Option 2: Pursuing a Chapter 13 Hardship Discharge

When a modification simply is not feasible because the income loss is both catastrophic and permanent, 11 U.S.C. § 1328(b) offers a different path: the Chapter 13 hardship discharge. This provision allows the court to discharge remaining eligible debts and close the repayment plan early—without requiring the debtor to complete all scheduled payments.

A hardship discharge is a meaningful legal protection, but the eligibility bar is deliberately high. Three mandatory criteria must all be satisfied simultaneously:

- The failure to complete payments must result from circumstances beyond the debtor’s reasonable control—such as a permanent disability or catastrophic illness—not from voluntary lifestyle decisions

- Creditors must have already received at least as much as they would have recovered under a Chapter 7 liquidation proceeding

- A plan modification must be completely impractical given the debtor’s current and projected financial situation

One critical limitation: a Chapter 13 hardship discharge does not wipe out every debt. Student loans, certain tax obligations, domestic support obligations, and secured debts where the debtor retains the collateral will survive this discharge. Debtors should enter this process with clear eyes about what relief it actually delivers.

Option 3: Convert Chapter 13 to Chapter 7

When a Chapter 13 income drop is so severe that no repayment—even a reduced one—is realistically possible, 11 U.S.C. § 348 and § 1307 permit the debtor to convert the existing case to a Chapter 7 liquidation. This is often described as the most powerful mid-case pivot available, as it can secure a relatively swift discharge of qualifying unsecured debts without any further plan payments.

Conversion is not without trade-offs. Weigh the following carefully before making this decision:

- ✅ Pro: Eliminates the obligation to make any further monthly plan payments

- ✅ Pro: Typically produces a much faster discharge—Chapter 7 cases often conclude within four to six months, compared to years remaining on a Chapter 13 plan

- ❌ Con: Non-exempt assets—including a home with substantial equity or a fully paid-off vehicle—become vulnerable to liquidation by the Chapter 7 trustee

- ❌ Con: The debtor must pass the Chapter 7 Means Test based on their new, lower income—though a genuine income drop often makes this easier to satisfy

A Note on State-Level Consumer Protection and Exemptions

While bankruptcy itself is governed by federal law, the assets protected from liquidation in a Chapter 7 conversion are determined almost entirely by state exemption statutes. This distinction matters enormously when evaluating whether conversion is the right move.

Consider how dramatically state law can shift the calculus:

- California operates a dual exemption system, requiring debtors to strategically choose between two distinct exemption sets to maximize protection of home equity and other assets

- Kansas and Nebraska maintain specific regional protections on wage garnishment and homestead equity that can shield more assets than the federal baseline

- Utah and Louisiana apply unique community property and asset protection rules that fundamentally alter the financial math of any Chapter 7 conversion

Visualizing the Mid-Case Crisis

The decision tree below maps the core legal pathways available to a Chapter 13 debtor facing a sudden income crisis. Use it as a starting framework before consulting legal counsel.

Option 4: Chapter 13 Dismissal – The Worst-Case Scenario

Ignoring a Chapter 13 income drop is not a neutral choice. It is a decision with serious, immediate legal consequences. National data consistently shows that approximately 33% of Chapter 13 cases are dismissed before completion, according to research published by the Federal Judicial Center—a figure that climbs sharply when debtors fail to respond proactively to financial disruption. Some district-level studies place local dismissal rates considerably higher.

A dismissal does not simply pause your bankruptcy—it dismantles the legal protections you entered the case to obtain:

- The automatic stay is lifted immediately, meaning foreclosure proceedings, vehicle repossessions, and wage garnishments can resume without delay

- Unpaid interest and late penalties on outstanding debts are applied retroactively from the date the original bankruptcy was filed

- The debtor becomes fully liable for all remaining balances, as if the bankruptcy case had never existed

If you have received a motion to dismiss from your trustee, the window to respond is narrow. Courts typically allow a short period to cure defaults or file a motion to modify—but that window closes fast.

Conclusion and Immediate Next Steps

A mid-case income drop is genuinely frightening. But it does not have to mean the end of your financial recovery. Federal law provides real, substantive options—plan modification, hardship discharge, and Chapter 7 conversion—each designed to address different levels of financial disruption. The critical variable in every scenario is time. Debtors who act quickly preserve options. Debtors who wait lose them.

Take these steps right now if your income has dropped during an active Chapter 13 case:

- Gather documentation immediately—recent pay stubs, termination letters, medical bills, or any formal proof of your income reduction

- Build an accurate picture of your current expenses—a bare-bones monthly budget that reflects only essential living costs

- Do not wait for the trustee to act—filing a motion to modify before a dismissal motion is filed puts you in a far stronger legal position

- Consult a qualified bankruptcy attorney as soon as possible—an experienced professional can run the numbers on modification versus conversion and identify which path best protects your assets and long-term financial health

The bankruptcy system was built with human unpredictability in mind. Use the protections it provides.

Frequently Asked Questions

Can I temporarily suspend my Chapter 13 payments if I lose my job?

There is no formal pause option in Chapter 13, but your attorney can file an emergency motion or negotiate a short-term deferral with the trustee. Act before you miss a payment.

How long does it take for a Chapter 13 plan modification to be approved?

In uncontested cases, approval typically takes four to eight weeks. Creditor objections can extend that timeline considerably.

What is the difference between a Chapter 13 hardship discharge and a standard Chapter 13 discharge?

A standard discharge is earned after completing all plan payments and covers more debts. A hardship discharge is granted early but is narrower in scope, mirroring Chapter 7 relief.

Will converting from Chapter 13 to Chapter 7 hurt my credit score more?

Converting does not restart the credit reporting clock – the original filing date still applies. A faster Chapter 7 resolution can actually help you begin rebuilding credit sooner.

Can my creditors object to a Chapter 13 plan modification?

Yes. Creditors and the trustee can file formal objections, which may trigger a court hearing and delay approval of your modified plan.

What happens to my cosigners if my Chapter 13 case is dismissed?

The codebtor stay lifts immediately upon dismissal, leaving your cosigners fully exposed to creditor collection actions on any shared debts.

Is it possible to refile Chapter 13 after a dismissal?

Yes, but the automatic stay in a new filing may be limited to just 30 days if you had a dismissal within the past year.

About The Author:

Lyle Solomon has extensive legal experience, in-depth knowledge, and experience in consumer finance and writing. He has been a member of the California State Bar since 2003. He graduated from the University of the Pacific’s McGeorge School of Law in Sacramento, California, in 1998 and currently works for the Oak View Law Group in California as a principal attorney.